Peer-To-Peer Lending: An Overview & It’s Working

Peer-to-Peer Lending: An Overview

Peer-to-peer (P2P) lending is an innovative financial model that connects borrowers directly with individual lenders through online platforms, bypassing traditional financial intermediaries like banks. This alternative form of lending has gained popularity due to its ability to offer competitive interest rates to borrowers while providing potentially higher returns to lenders compared to conventional savings or investment products.

How Peer-to-Peer Lending Works

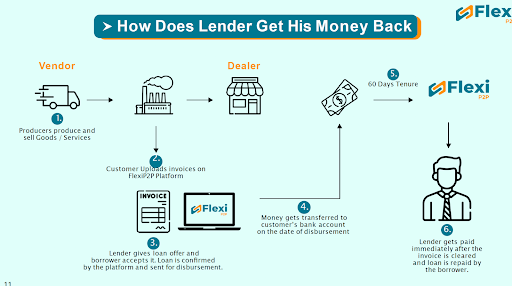

P2P lending platforms operate as online marketplaces where borrowers seeking loans can post their requirements, and lenders can choose to fund these loans, either fully or partially. The process typically involves the following steps:

- Borrower Application: A borrower submits a loan application detailing the amount needed, purpose of the loan, and financial background.

- Risk Assessment: The P2P platform evaluates the borrower’s creditworthiness, often assigning a risk grade or interest rate based on the borrower’s credit score, income, and other financial indicators.

- Loan Listing: Approved loans are listed on the platform’s marketplace, where potential lenders can review and choose to invest in the loan.

- Funding: Multiple lenders can contribute to funding a single loan. Once the loan is fully funded, the borrower receives the money.

- Repayment: Borrowers repay the loan in installments over time, and lenders receive their share of the repayments, including interest, in proportion to their investment.

Benefits of Peer-to-Peer Lending

- Access to Capital: P2P lending provides an alternative source of credit for borrowers who may not qualify for traditional bank loans due to lower credit scores or other factors.

- Higher Returns: For lenders, P2P lending can offer higher returns compared to traditional savings accounts or bonds, as they earn interest on the loans they fund.

- Diversification: Lenders can diversify their risk by spreading their investments across multiple loans with different risk profiles.

- Transparency: P2P platforms provide detailed information about borrowers, loan terms, and expected returns, allowing lenders to make informed investment decisions.

Risks of Peer-to-Peer Lending

- Default Risk: The primary risk for lenders is the potential for borrower default. P2P loans are typically unsecured, meaning there is no collateral to recover in case of non-payment.

- Platform Risk: The stability and reliability of the P2P platform itself can be a risk, especially if the platform lacks sufficient regulatory oversight or financial backing.

- Liquidity Risk: P2P loans are generally not tradable or liquid, meaning lenders may not be able to withdraw their funds before the loan term ends.

The Future of Peer-to-Peer Lending

As the P2P lending industry matures, platforms are increasingly adopting more sophisticated risk assessment tools, including AI and machine learning, to better evaluate borrower creditworthiness and reduce default rates. Additionally, regulatory frameworks are evolving to provide more protection for both borrowers and lenders. Luckily in India, the Reserve Bank of India has been very proactive and has laid down a comprehensive regulatory framework for Peer to Peer Lending – yielding comfort to lenders and borrowers alike.

Peer-to-peer lending is positioned to play a significant role in the future of finance, offering an accessible, flexible, and potentially lucrative alternative to traditional lending and investment models. However, participants must carefully consider the associated risks and conduct thorough research before engaging in P2P lending activities.